Tata Motors Passenger Vehicles Share Falling: 7 Real Reasons Investors Are Worried In 2026

Tata Motors Passenger Vehicles Share Falling: 7 Real Reasons Investors Are Worried In 2026 | Image Via © tatamotors.com

If you track Tata Motors Passenger Vehicles share lately, you see something feels off. The stock declines nearly 18 to 22 percent from its recent highs and repeatedly tests levels close to its 52 week low. Naturally, the big question everyone asks is simple, why Tata Motors passenger vehicles share falling despite strong sales in India?

The interesting part is, this is not a simple story of a weak company. It is more like a mix of strong domestic growth and global challenges. On one side, Tata Motors India business reports steady volume growth of around 8 to 10% yoy, while on the other side, its global arm Jaguar Land Rover contributes nearly 70 to 80 percent of total revenue and faces operational disruptions and margin pressure.

Because of this contrast, many investors stay stuck between optimism and frustration. Recent developments such as production halts, supply chain issues, and reported financial losses add more uncertainty, making the overall outlook look confusing despite strong fundamentals in the domestic segment.

Key Takeaways On Tata Motors Share Fall

- Tata Motors PV share is falling mainly due to JLR-related problems

- Jaguar Land Rover contributes ~70-80% of total revenue

- Recent production halts and past cyberattack hit earnings badly

- Weak global demand, especially in China and Europe

- High debt and negative cash flow are worrying investors

- Indian PV business is strong but not enough to offset global losses

- Market sentiment is currently negative but long-term outlook is mixed

Table of Contents

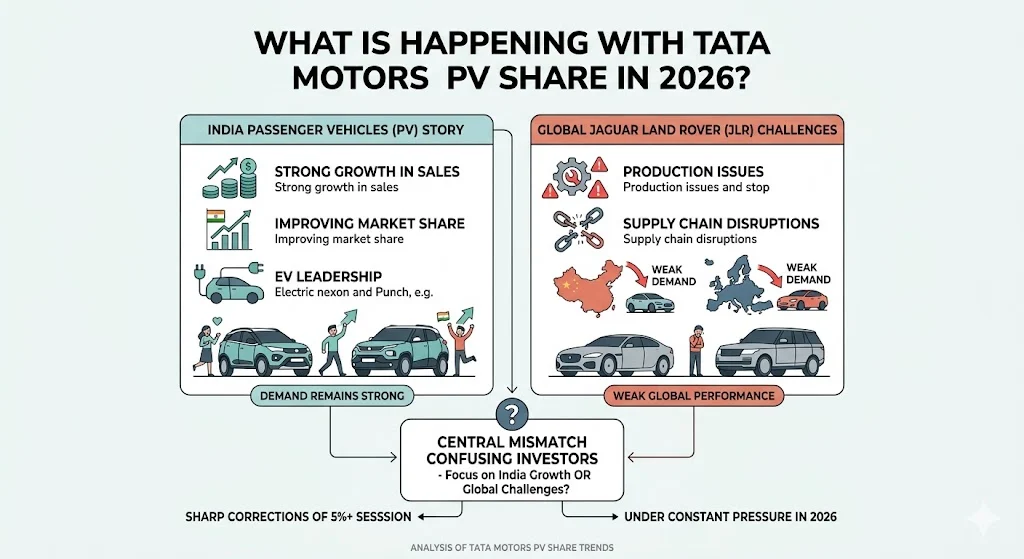

What Is Happening With Tata Motors PV Share?

Tata Motors Passenger Vehicles share has been under constant pressure in 2026. The stock has seen multiple sharp corrections, including drops of 5% or more in a single session. This kind of movement is not normal for a fundamentally strong company, which is why many investors are trying to understand the real reason behind this trend.

The biggest reason behind this fall is not technical. It is fundamentally driven. This means the issue is not related to charts or short-term trading patterns. Instead, it is linked to the company’s overall business performance and future outlook. Investors are reacting to real concerns about earnings, growth, and stability.

The company is currently facing what can be called a “two different business story” situation. On one side, its India passenger vehicle business is performing well. Sales are growing, market share is improving, and the company is doing well in the electric vehicle segment. Models like Nexon and Punch are popular, and demand remains strong.

However, on the other side, its global luxury arm Jaguar Land Rover is struggling. JLR is facing production issues, supply chain disruptions, and weak demand in key markets like China and Europe. Since JLR contributes a large portion of Tata Motors’ total revenue, any weakness there directly impacts the overall financial performance.

This mismatch between strong domestic growth and weak global performance is exactly what is confusing investors right now. They are unsure whether to focus on the positive India story or the negative global challenges. This uncertainty is leading to selling pressure and keeping the stock under stress.

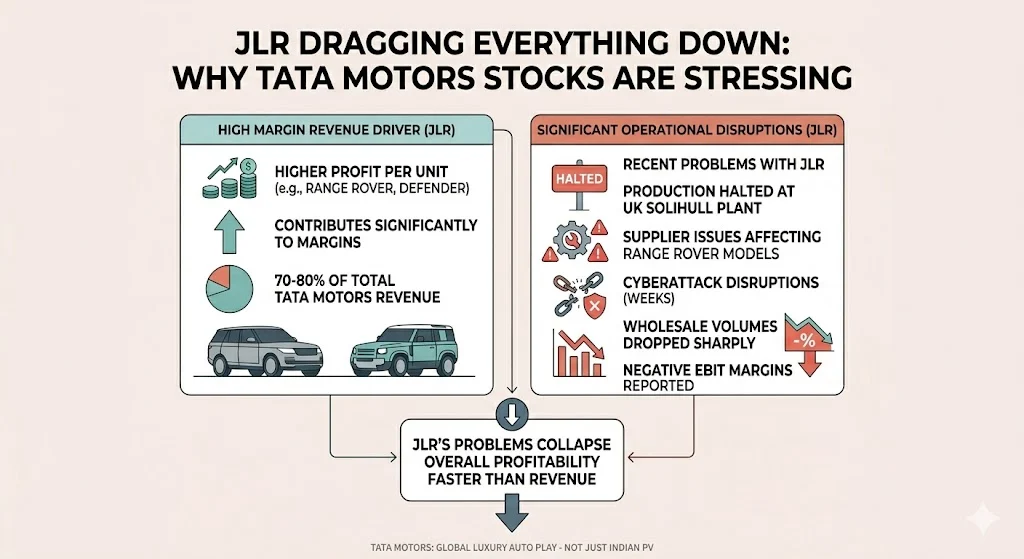

The Biggest Reason: JLR Is Dragging Everything Down

Let’s be real. The entire Tata Motors story today depends heavily on Jaguar Land Rover. JLR contributes around 70-80% of total revenue. So even a small problem there creates a big impact on the overall stock. This is why analysts often say Tata Motors is more of a global luxury auto play than just an Indian passenger vehicle company.

To understand the impact better, you need to look at how JLR drives profitability. While India business contributes volume, JLR contributes margins. Luxury vehicles like Range Rover and Defender generate higher profit per unit. So when JLR struggles, overall profitability collapses much faster than revenue.

Recent Problems With JLR

- Production halted at UK Solihull plant

- Supplier issues affecting Range Rover models

- Earlier cyberattack disrupted operations for weeks

- Wholesale volumes dropped sharply

- Negative EBIT margins reported

These are not small issues. These directly hit revenue, margins, and investor confidence.

Let’s break this down further. Production halts mean delayed deliveries, which directly impacts quarterly numbers. Supplier issues create bottlenecks, especially for high-demand models like Range Rover, leading to lost sales opportunities. The cyberattack earlier disrupted backend systems, affecting logistics and order processing.

At the same time, falling wholesale volumes indicate weak demand or supply constraints, both of which are negative signals. Negative EBIT margins are even more concerning because they show the company is not making operational profits in that segment.

Another important factor is brand positioning. JLR operates in the premium segment, where customer expectations are very high. Any delay, quality issue, or supply disruption can damage brand perception, which takes time to recover.

When investors see repeated disruptions, they lose trust in near-term recovery. That’s exactly what is happening now.

Weak Global Demand Is Making Things Worse

Even without disruptions, JLR was already facing demand problems, and this issue is deeper than it looks on the surface. The global luxury automobile market is going through a structural shift, where traditional premium brands are struggling to adapt quickly enough to changing consumer preferences and technological disruption.

Key Global Issues

- China luxury car demand slowing down

- Strong competition from EV players

- High taxes on premium cars

- Rising costs in Europe and US

- Expensive EV transition

China, which was once the biggest growth engine for luxury carmakers, is no longer as reliable as before. Local EV brands like BYD, NIO, and Li Auto are offering advanced technology, better pricing, and strong government support. These companies are not just competing on price but also on innovation, which is attracting younger buyers. As a result, JLR’s traditional luxury positioning is losing its edge in this crucial market.

In addition to China, demand softness is also visible in parts of Europe due to economic uncertainty and high inflation. Consumers are becoming more cautious with big-ticket purchases like luxury vehicles. At the same time, interest rates remain elevated in many regions, making financing expensive for buyers.

Another major challenge is the rising cost structure. Regulatory pressure in Europe and the US is forcing automakers to invest heavily in emission compliance and electrification. This includes stricter carbon norms, safety regulations, and sustainability requirements. These factors are significantly increasing production costs.

The transition to electric vehicles is also capital-intensive. Developing EV platforms, battery technology, and charging ecosystems requires massive investment. For JLR, this transition is happening while its core ICE (internal combustion engine) business is already under pressure.

So even if sales volumes remain stable or slightly improve, profitability continues to suffer due to higher costs, pricing pressure, and intense competition.

Financial Stress & Rising Debt Concerns

Another major red flag is financial performance, and this is where investors are becoming increasingly cautious. While Tata Motors has shown strong growth in its domestic passenger vehicle segment, the overall financial health of the company is still under pressure due to global challenges, especially from JLR.

The company has reported losses in recent quarters, which directly impacts investor confidence. At the same time, debt levels remain significantly high, creating concerns about long-term sustainability and financial flexibility.

Financial Snapshot

| Metric | Situation |

|---|---|

| Net Profit | Negative in recent quarters |

| Debt | Around ₹39,000+ crore |

| Cash Flow | Negative |

| Margins | Under pressure |

But to understand the seriousness of the situation, we need to go a bit deeper.

Why High Debt Is A Concern

- High interest payments reduce overall profitability

- Limits the company’s ability to invest aggressively in EV and future technologies

- Makes the company more vulnerable during global slowdowns

- Increases dependency on consistent cash flow from JLR

When a company carries heavy debt, even small disruptions in revenue can create a big impact on financial stability. This is exactly what investors are worried about right now.

Cash Flow Pressure Is A Bigger Issue

Negative cash flow is often considered more dangerous than temporary losses. It means the company is not generating enough cash from operations to sustain itself comfortably.

In simple terms, even if a company shows revenue growth, it still needs actual cash inflow to run daily operations, pay suppliers, service debt, and invest in future growth. When cash flow turns negative, it creates a liquidity stress situation.

This forces companies to either:

- Borrow more money

- Cut down investments

- Delay expansion plans

None of these are positive signals for long-term growth.

Additionally, persistent negative cash flow can impact credit ratings, increase borrowing costs, and reduce financial flexibility. For a capital-intensive business like Tata Motors, especially with global operations like JLR, maintaining healthy cash flow is critical. If this issue continues for multiple quarters, it can start affecting strategic decisions and long-term competitiveness.

Margin Pressure Adds To The Problem

Margins are under pressure due to rising input costs, supply chain disruptions, and global competition. Even if sales remain stable, lower margins mean reduced profitability.

Several factors are contributing to this margin squeeze:

- Higher raw material costs (steel, aluminum, semiconductors)

- Increased logistics and transportation expenses

- Currency fluctuations impacting import/export costs

- Heavy investments in EV technology and R&D

When margins shrink, companies earn less profit per vehicle sold. This directly impacts earnings per share (EPS), which is a key metric investors track closely.

Investor Perspective

This combination high debt, negative cash flow, and weak margins creates a risk-heavy profile. High debt + falling profits = higher risk

From an investor’s point of view, this raises multiple concerns:

| Risk Factor | Impact |

|---|---|

| High Debt | Increased interest burden |

| Negative Cash Flow | Liquidity stress |

| Weak Margins | Lower profitability |

That’s why even long-term investors are cautious right now. Until there is clear improvement in cash flow stability and margin expansion, confidence in the stock may remain limited.

Market Sentiment & Demerger Impact

After the demerger of passenger vehicles business, something unexpected happened. The stock started behaving like an “orphan stock”.

This term is often used in the market when a company or segment gets separated but does not immediately find strong institutional backing or clear valuation benchmarks. In Tata Motors’ case, the demerger created a situation where investors were unsure how to value the standalone passenger vehicle business versus the global JLR operations.

What Does That Mean

- Institutional selling pressure increased

- Algorithmic trading created volatility

- Valuation confusion among investors

Let’s break this down further.

After the demerger, many large institutional investors and mutual funds had to rebalance their portfolios. Some funds exited or reduced exposure because the new structure did not fit their investment mandate. This created consistent selling pressure in the market.

At the same time, algorithmic and high-frequency trading systems picked up on the volatility and uncertainty. These systems often amplify short-term price movements, leading to sharp ups and downs even without major fundamental changes.

Another major issue is valuation confusion. Investors are struggling to decide whether Tata Motors should be valued as a domestic auto company, a global luxury car player, or a mix of both. Each segment has different valuation multiples, making it difficult to arrive at a fair price.

Additionally, the lack of clear communication or guidance post-demerger has added to uncertainty. When investors don’t have clarity, they tend to stay cautious or avoid fresh buying.

Even though valuations look cheap on paper, sentiment is weak. And in the stock market, sentiment matters a lot in the short term.

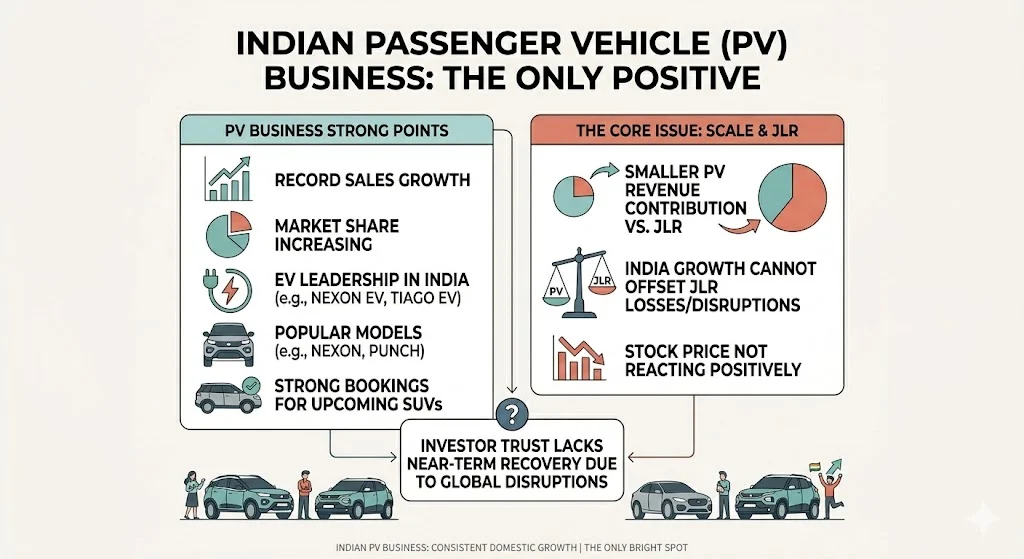

Indian Passenger Vehicle Business: The Only Positive

Now comes the surprising part.

Tata Motors India business is actually doing very well, and in fact, it is one of the strongest pillars supporting the company right now. While global operations are facing challenges, the domestic passenger vehicle (PV) segment continues to show consistent growth, innovation, and strong consumer demand.

Strong Points

- Record sales growth

- Market share increasing

- EV leadership in India

- Popular models like Nexon and Punch

- Strong bookings for upcoming SUVs

Over the past few years, Tata Motors has successfully repositioned itself as a premium yet value-driven brand in India. Models like Nexon, Punch, and Harrier have gained massive popularity due to their safety ratings, design, and feature-rich offerings. This has helped the company steadily increase its market share in a highly competitive segment.

The company has even crossed 200,000+ retail numbers in some periods, which clearly shows strong demand momentum. Additionally, Tata Motors has built a strong presence in Tier 2 and Tier 3 cities, expanding its reach beyond metro markets.

One of the biggest strengths of Tata Motors India business is its leadership in the EV segment. With models like Nexon EV and Tiago EV, the company has captured a significant share of India’s electric vehicle market. Government incentives, rising fuel prices, and increasing awareness are further boosting EV adoption.

EV segment is growing fast, with strong YoY growth, and Tata Motors is currently ahead of most competitors in terms of early mover advantage. However, the core issue remains scale.

Despite strong domestic performance, the India PV business contributes a smaller portion of overall revenue compared to JLR. This means even strong growth in India is not enough to offset losses or disruptions in the global luxury segment. That’s why stock is not reacting positively despite good domestic performance.

Public Opinion: What People Are Saying On Twitter

When you check X (Twitter), you will see very mixed reactions.

Negative Sentiment

- Frustration over repeated JLR issues

- Anger on management decisions

- Concerns about global strategy

Positive Views

- Strong belief in India business growth

- Excitement around new launches like Sierra

- Confidence in EV leadership

- Some investors calling it a “buy on dips” opportunity

So overall sentiment is confused. Short-term traders are bearish Long-term investors are divided

Why Stock Is Falling Even When Valuation Looks Cheap

Many people are asking this question. If stock is cheap, why is it still falling? Here’s the simple answer: Cheap stocks can become cheaper if uncertainty is high. Right now, there are too many unknowns:

- When will JLR fully recover

- How global demand will behave

- Whether margins will improve

- How debt will be managed

But there is more to this story. Valuation alone does not decide stock movement. Investors also look at future visibility and risk. If future earnings are not clear, even a low valuation does not attract strong buying. Another important factor is earnings consistency. Tata Motors has shown uneven performance in recent quarters. Some quarters show improvement, while others show losses. This creates doubt in the minds of investors.

Also, institutional investors play a big role. When big funds reduce their exposure, stock price falls even if valuation looks attractive. Retail investors usually follow this trend. Let’s understand this better:

| Factor | Impact on Stock |

|---|---|

| Low valuation | Attracts buyers only if growth is visible |

| Uncertain earnings | Creates fear among investors |

| High debt | Increases financial risk |

| Global exposure | Adds external risks |

Another reason is opportunity cost. Investors compare Tata Motors with other auto stocks. If other companies show stable growth and better margins, money shifts there.

Market psychology also matters. When a stock keeps falling, many investors avoid it. They wait for clear signs of recovery before entering again. So even if the stock looks cheap on paper, lack of confidence keeps it under pressure. Until these questions get clarity, stock may remain under pressure.

Future Outlook: What Can Change The Trend

The future of Tata Motors PV share depends on a few key triggers.

Positive Triggers

- JLR production normalization

- Improvement in global demand

- Better margins in coming quarters

- Strong success of new launches

- Continued EV growth in India

Negative Risks

- More supply chain disruptions

- Weak China demand

- Rising global costs

- Geopolitical tensions

So clearly, this is not a one-direction story.

Final Verdict

Tata Motors Passenger Vehicles share is falling mainly because of JLR problems, not because the entire company is weak. India business is actually doing great, but global issues are overshadowing it. For short term, volatility will likely continue.

For long term, everything depends on how fast JLR stabilizes and whether India business scales up strongly. Right now, this stock is a classic case of high potential but high uncertainty.

Related Posts :

Share This Post