Best Metal & Mining Dividend Stocks in India 2026: High Yield, Deep Analysis, and Smart Income Strategy

Best Metal & Mining Dividend Stocks in India 2026

Metal and mining dividend stocks in India are gaining strong attention in 2026. The reason is simple. Investors are looking for both income and growth at the same time. In volatile markets, dividend-paying stocks provide stability. And in a sector like metals, strong cash flows make high dividends possible.

But most articles only give a list of stocks. They do not explain why these companies pay high dividends. They do not explain risks. And they do not give real insights backed by numbers.

In this detailed guide, you will get everything. You will understand each major metal and mining dividend stock in depth. You will see numeric data, dividend trends, business strengths, risks, and latest news. This is not just a list. This is a complete research-backed guide for serious investors.

Key Takeaways

- Metal stocks offer both dividend income and cyclical growth opportunities.

- PSU companies like Coal India and NMDC provide stable and consistent payouts.

- Vedanta and Hindustan Zinc offer very high yields but require careful risk understanding.

- Commodity prices directly impact dividends in this sector.

- A diversified approach is important due to sector volatility.

Table of Contents

Why Metal & Mining Companies Pay High Dividends

Dividend comes from profit. And metal companies generate strong profits during commodity upcycles. These companies benefit from:

- Low production cost in India

- High global demand for metals

- Strong operating margins

- Large-scale production capacity

PSU companies also play a key role. They often distribute a large portion of profits as dividends. This makes them attractive for income investors. However, this sector is cyclical. That means profits and dividends can change based on global prices.

Top Metal & Mining Dividend Stocks in India (2026)

| Company Name | Dividend Yield Range | Key Strength |

|---|---|---|

| Vedanta Ltd | 6% – 9%+ | High payouts, diversified metals |

| Coal India Ltd | 5.8% – 6.9% | Stable cash flow, monopoly |

| Hindustan Zinc | 5.6% – 6.6% | High ROE, strong margins |

| NMDC Ltd | 4% – 4.5% | PSU stability, iron ore leader |

These companies dominate dividend discussions in 2026.

Detailed Stock Analysis with Numeric Data and Insights

1) Vedanta Ltd – High Yield King with Risk

Vedanta is one of the highest dividend-paying companies in India.

Dividend Yield

Around 6% to 9% depending on payouts and stock price. In certain years, Vedanta has even delivered double-digit effective yields due to multiple interim dividends. This makes it one of the most attractive income-generating stocks in India, especially for investors seeking regular cash flow.

Dividend Trend

- Multiple interim dividends every year

- Aggressive payout strategy

- Vedanta follows a unique dividend policy where it distributes profits frequently rather than waiting for annual payouts. Over the past few years, the company has consistently rewarded shareholders with quarterly or even more frequent dividends. This approach improves liquidity for investors and makes it a preferred choice for dividend-focused portfolios.

Financial Insights

- Revenue comes from zinc, aluminium, oil, iron ore

- High EBITDA margins in key segments

- Debt levels are relatively high compared to peers

- Vedanta operates as a diversified natural resources company, which helps reduce dependency on a single commodity. Its zinc business, through Hindustan Zinc, contributes significantly to profitability with industry-leading margins.

- Aluminium and oil segments also generate strong cash flows during favorable commodity cycles. However, the company carries a relatively high debt burden, which remains a key concern for long-term investors.

Latest News and Insights

- Vedanta is planning a major demerger. The company aims to split into multiple business units. This could unlock value for shareholders by allowing each segment to be valued independently. However, the restructuring process may create short-term uncertainty and volatility in stock price.

- Additionally, global commodity prices remain supportive, especially for zinc and aluminium, which strengthens Vedanta’s earnings outlook. Strong operational performance continues to support its high dividend payouts.

- High dividends are supported by strong cash flow. But investors must monitor debt levels carefully, as rising interest costs or weaker commodity prices could impact future payouts.

Investor Insight

Best suited for high-income investors who can handle volatility and are comfortable with cyclical risks.

2) Coal India Ltd – The Stability Leader

Coal India is one of the most reliable dividend stocks in India, especially for investors who prioritize steady income and capital safety.

Dividend Yield

Around 5.8% to 6.9%

Coal India’s dividend yield consistently ranks among the highest in the PSU segment. This is driven by its strong and predictable cash generation along with a government-backed dividend distribution policy. The company typically maintains a high payout ratio, making it a preferred choice for income-focused investors who want regular returns without excessive risk.

Dividend Track Record

₹5.50 dividend in early 2026

₹10+ dividend in late 2025

Coal India has a well-established history of paying both interim and final dividends multiple times within a financial year. Over the past few years, the company has maintained a payout ratio often exceeding 70% of its net profit. This reflects a strong commitment to shareholder returns and makes it one of the most consistent dividend-paying companies in India.

Financial Strength

- Near monopoly in coal production

- Zero or very low debt

- Strong free cash flow

Coal India operates with a dominant position in India’s coal mining sector, supplying more than 80% of the country’s coal requirements. Its balance sheet is exceptionally strong, with minimal debt and significant cash reserves. The company benefits from high operating margins and stable demand, which ensures consistent free cash flow generation. This financial strength directly supports its ability to sustain high dividend payouts even during economic fluctuations.

Operational Strength

- Produces majority of India’s coal

- Consistent production growth

Coal India continues to expand its production capacity to meet rising domestic energy demand. With India’s electricity consumption steadily increasing, the company plays a crucial role in maintaining energy security. Its large-scale mining operations, extensive distribution network, and logistical efficiency provide a strong competitive advantage that is difficult for new entrants to replicate.

Latest Industry Developments

Coal demand remains strong due to power sector dependency. Despite renewable energy growth, coal continues to remain critical for India’s energy needs.

Government policies are actively supporting domestic coal production to reduce reliance on imports. While renewable energy is growing rapidly, thermal power still forms the backbone of India’s energy infrastructure. This ensures sustained long-term demand for Coal India’s output, reinforcing its revenue stability.

Investor Insight

Coal India is ideal for conservative investors looking for stable and predictable income. For investors seeking consistent cash flow with relatively lower volatility, Coal India stands out as a dependable dividend stock. Its strong fundamentals, dominant market position, government backing, and reliable dividend history make it a core holding for long-term income-focused portfolios.

3) Hindustan Zinc Ltd – Profitability Powerhouse

Hindustan Zinc is one of the most efficient companies in the sector and is often considered a benchmark for profitability in the Indian mining space. Its operational efficiency, cost leadership, and strong parent backing from Vedanta Group make it a standout performer among dividend-paying metal stocks.

Dividend Yield

- Around 5.6% to 6.6

- The company has consistently rewarded shareholders with high dividends, supported by strong cash generation and disciplined capital allocation.

Return Ratios

- ROE above 70%

- Very high ROCE

- These exceptional return ratios indicate that the company is highly efficient in using shareholder capital and generating profits from its assets. Few companies in India maintain such consistently high returns over long periods.

Financial Strength

- Low debt

- Strong margins in zinc and silver

- Hindustan Zinc operates with minimal leverage, which reduces financial risk. Its EBITDA margins are among the highest in the global mining industry, often exceeding 50%, driven by low-cost production and high-grade reserves.

Business Insight

Zinc demand is rising due to infrastructure and industrial use. It is widely used in galvanization, which protects steel from corrosion. With India’s infrastructure push and global construction recovery, zinc demand is expected to remain strong. Silver demand is also increasing due to renewable energy applications, especially in solar panels and electronics.

Latest News

Global zinc prices are stable, providing earnings visibility. Silver demand is rising with EV and solar growth, which is a positive trigger for future profitability. The company is also investing in capacity expansion and exploration to sustain long-term production growth.

Investor Insight

A strong combination of high dividend and strong fundamentals. Suitable for investors looking for both income and long-term value creation with relatively lower risk compared to other high-yield metal stocks.

4) NMDC Ltd – Balanced PSU Pick

NMDC is a government-owned iron ore producer and one of the largest iron ore mining companies in India. It plays a critical role in supplying raw material to the domestic steel industry, making it an important part of India’s infrastructure growth story.

Dividend Yield: Around 4% to 4.5%

Financial Data

- Stable revenue from iron ore

- Moderate growth profile

- Strong balance sheet with low debt levels

- Consistent operating margins supported by efficient mining operations

NMDC has historically maintained a healthy dividend payout ratio, often distributing a significant portion of its profits to shareholders. Its strong cash flow generation allows it to sustain dividends even during moderate downturns in commodity prices.

Business Insight

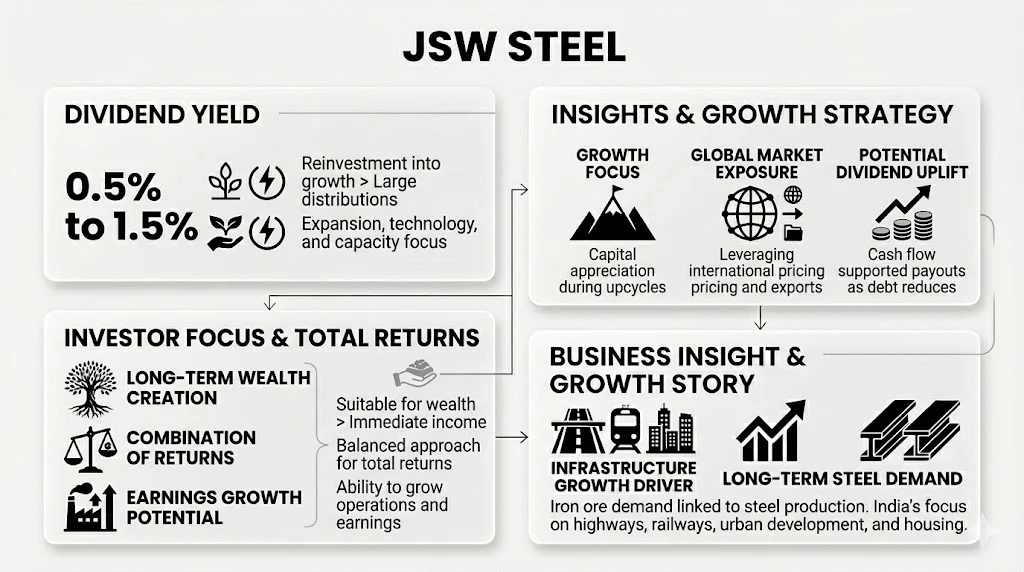

Iron ore demand depends heavily on steel production. As infrastructure projects increase, steel demand rises, which directly boosts iron ore consumption. India’s focus on highways, railways, urban development, and housing continues to support long-term demand for iron ore.

Additionally, NMDC benefits from its low-cost mining operations, which gives it a competitive advantage even when global iron ore prices fluctuate. This cost efficiency helps protect margins and ensures steady profitability.

Latest News

The government’s continued push on infrastructure spending is supporting iron ore demand. NMDC is also expanding its production capacity and exploring new mining projects to meet future demand. There are ongoing discussions around strategic disinvestment, which could unlock value for shareholders in the long term.

Investor Insight

NMDC is suitable for investors who prefer stability over aggressive growth. It offers a balanced combination of moderate dividend yield and steady business performance. While it may not deliver very high returns like cyclical metal stocks, it provides consistency and lower risk, making it a good addition to a diversified dividend portfolio.

Growth Stocks with Dividend Potential

Some companies do not offer very high yield but provide growth plus dividend. These stocks are important for investors who want a balance between income and long-term wealth creation. While their dividend payouts may appear lower compared to high-yield PSU stocks, their ability to grow earnings over time can lead to higher total returns. In many cases, these companies reinvest a significant portion of their profits into expansion, technology upgrades, and global acquisitions. This strategy helps them increase future profitability, which can eventually lead to higher dividends as well.

1) Tata Steel

- Dividend Yield Around 1% to 2%

- Focus: Expansion and global operations

- Insight: Better for capital appreciation than income.

Tata Steel is one of India’s largest steel producers with a strong global presence across Europe and Southeast Asia. The company has consistently focused on improving operational efficiency and reducing debt, especially after its major acquisitions in the past decade. Its revenue is diversified across domestic and international markets, which helps reduce dependency on a single geography.

From a financial perspective, Tata Steel has shown strong EBITDA margins during favorable steel cycles. The company also benefits from backward integration, which helps control raw material costs. Although the dividend yield remains modest, Tata Steel has a history of rewarding shareholders during strong profit cycles with higher payouts.

Recent developments indicate that the company is investing heavily in green steel initiatives and sustainability projects. This aligns with global trends and could improve long-term competitiveness. Additionally, infrastructure growth in India continues to support steel demand, which directly benefits Tata Steel’s core business.

For investors, Tata Steel represents a growth-oriented dividend stock. It may not provide high immediate income, but it offers strong potential for capital appreciation along with periodic dividend rewards.

2) JSW Steel

Dividend Yield

Low but consistent, typically ranging between 0.5% to 1.5% depending on market conditions and company profitability. While this may appear modest compared to high-yield PSU stocks, it reflects a strategic approach where companies prioritize reinvestment into expansion, capacity building, and technological upgrades rather than distributing large portions of profits as dividends.

Also Read: JSW Steel Share Price Target

Insight

Strong growth focus with occasional dividends. Companies in this category, such as JSW Steel, are aggressively expanding their production capacity and strengthening their global footprint. This growth-oriented strategy allows them to benefit significantly during commodity upcycles, leading to capital appreciation for investors.

Additionally, these companies maintain financial discipline by balancing debt and operational efficiency. Their dividend payouts, although not very high, are supported by improving cash flows and better margin management. Over time, as expansion projects stabilize and debt reduces, there is potential for higher dividend payouts.

Another important factor is their exposure to global markets. Unlike PSU companies that rely heavily on domestic demand, these firms benefit from international pricing trends, export opportunities, and diversified revenue streams. This adds an extra layer of growth potential.

For investors, these stocks are more suitable for long-term wealth creation rather than immediate income generation. The combination of steady dividends and strong earnings growth can lead to better total returns over time.

In summary, while the dividend yield may be low, the real value lies in the company’s ability to grow earnings, expand operations, and eventually enhance shareholder returns through both price appreciation and gradually increasing dividends.

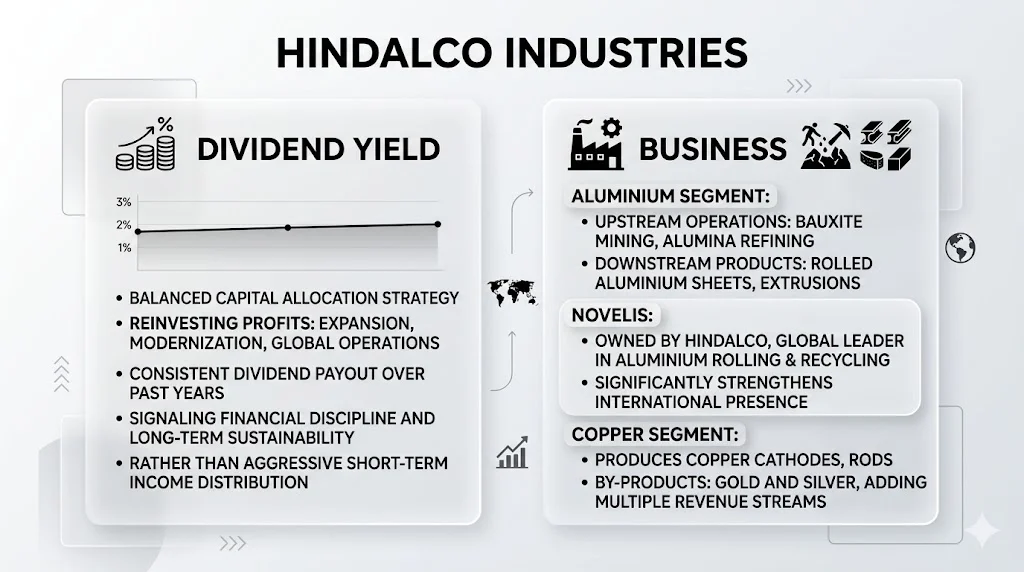

3) Hindalco Industries

Dividend Yield

Around 1% to 2%, which may appear modest compared to high-yield PSU stocks, but it reflects a more balanced capital allocation strategy. Hindalco focuses on reinvesting profits into expansion, modernization, and global operations rather than distributing a large portion as dividends. Over the past few years, the company has maintained a consistent dividend payout, signaling financial discipline and long-term sustainability rather than aggressive short-term income distribution.

Business

Hindalco operates across aluminium and copper segments, making it one of the most diversified metal companies in India. Its aluminium business includes upstream operations like bauxite mining and alumina refining, as well as downstream products such as rolled aluminium sheets and extrusions. The company also owns Novelis, a global leader in aluminium rolling and recycling, which significantly strengthens its international presence. In the copper segment, Hindalco produces copper cathodes, rods, and by-products like gold and silver, adding multiple revenue streams.

Insight

Hindalco benefits strongly from rising global aluminium demand, especially driven by sectors like electric vehicles, renewable energy, packaging, and infrastructure. Aluminium is increasingly preferred due to its lightweight and recyclable properties, making it critical for sustainability-focused industries. Additionally, Novelis plays a key role in supplying aluminium to global automotive giants, positioning Hindalco as a major player in the EV supply chain. While dividend yield is lower, the company offers strong growth potential, improving margins, and global exposure, making it suitable for investors who want a mix of moderate income and long-term capital appreciation.

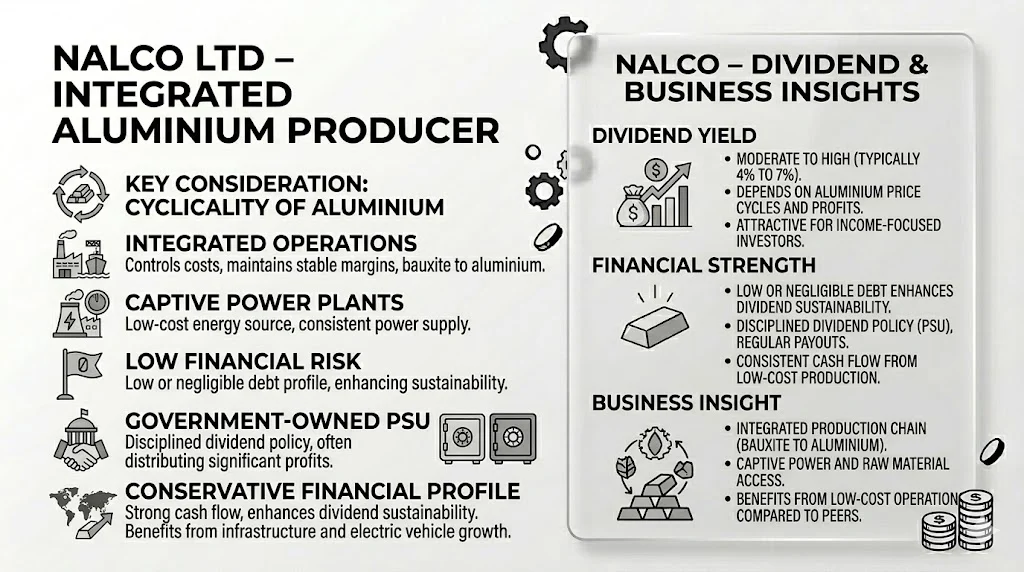

4) NALCO

Dividend Yield

Moderate to high, typically ranging between 4% to 7% depending on aluminium price cycles and company profitability. NALCO has historically maintained a strong dividend payout ratio, often distributing a significant portion of its profits to shareholders. This makes it an attractive option for income-focused investors, especially during favourable commodity cycles when earnings are strong.

Insight

NALCO (National Aluminium Company Limited) is a government-owned aluminium producer with integrated operations, including bauxite mining, alumina refining, and aluminium smelting. This integrated structure helps control costs and maintain stable margins compared to peers. The company benefits from low-cost production due to captive power plants and access to raw materials, which supports consistent cash flow generation.

One of the key strengths of NALCO is its conservative financial profile. It typically operates with low or negligible debt, which enhances dividend sustainability even during weaker commodity cycles. Additionally, being a PSU, it often follows a disciplined dividend policy aligned with government expectations, ensuring regular payouts.

From a sector perspective, aluminium demand is expected to grow due to increasing usage in infrastructure, electric vehicles, renewable energy, and packaging industries. This long-term demand outlook supports NALCO’s earnings visibility.

However, investors should also consider that aluminium prices are highly cyclical and influenced by global factors such as China’s production levels, energy costs, and international demand. This means dividend payouts can fluctuate based on market conditions.

Overall, NALCO offers a balanced combination of moderate-to-high dividend yield, financial stability, and exposure to long-term aluminium demand growth, making it a suitable addition for investors seeking steady income with moderate risk.

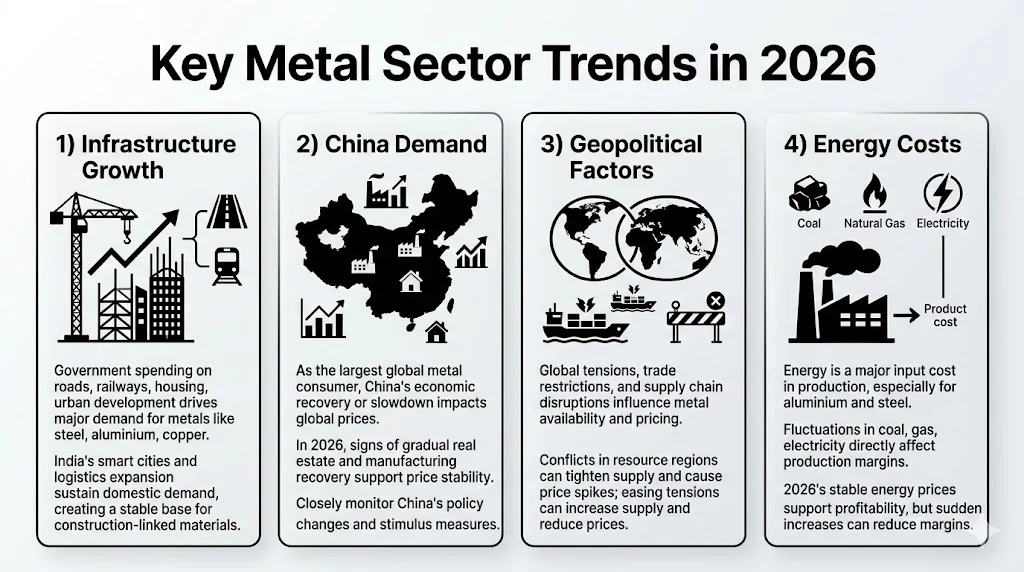

Key Sector Trends in 2026

Metal sector in 2026 is influenced by several factors, and understanding these drivers is essential for investors who want to make informed decisions in this cyclical industry.

1) Infrastructure Growth

Government spending on roads, railways, housing, and urban development continues to be a major demand driver for metals like steel, aluminium, and copper. India’s ongoing infrastructure push under initiatives such as smart cities and logistics expansion is expected to sustain domestic demand. This creates a stable base for metal companies, especially those focused on construction-linked materials.

2) China Demand

China remains the largest consumer of metals globally. Any recovery or slowdown in its economy directly impacts global metal prices. In 2026, signs of gradual recovery in China’s real estate and manufacturing sectors are supporting price stability. However, investors must closely monitor policy changes and stimulus measures from China, as they can quickly shift global demand dynamics.

Geopolitical Factors

Global tensions, trade restrictions, and supply chain disruptions continue to influence metal availability and pricing. Conflicts in resource-rich regions or export restrictions by major producers can tighten supply, leading to price spikes. At the same time, easing tensions can increase supply and reduce prices, making this factor highly unpredictable.

Energy Costs

Energy is a major input cost in metal production, especially for aluminium and steel. Fluctuations in coal, gas, and electricity prices directly affect production margins. In 2026, relatively stable energy prices are supporting profitability, but any sudden increase can quickly reduce margins for producers.

Overall, these factors create a dynamic environment where opportunities and risks coexist. Investors who track these macro trends can better anticipate price movements and make smarter investment decisions in the metal sector.

Dividend Sustainability Analysis

High dividend does not always mean safe dividend. Many investors get attracted to high yields without understanding whether the company can actually sustain those payouts over time. In cyclical sectors like metals and mining, this becomes even more important because profits can fluctuate significantly based on global demand and commodity prices.

Important checks:

1) Payout Ratio: Should not be extremely high

A payout ratio above 80–90% may indicate that the company is distributing most of its earnings instead of reinvesting in the business. While this may look attractive in the short term, it can limit future growth and make dividends vulnerable during downturns. A balanced payout ratio ensures both shareholder returns and business sustainability.

2) Free Cash Flow: Must support dividend payments

Dividends are paid from cash, not just accounting profits. A company may show strong net profit but still struggle with cash flow due to high capital expenditure or working capital requirements. Consistent positive free cash flow is a strong indicator that dividends are backed by real earnings.

3) Debt Levels: High debt can reduce future payouts

Companies with high debt obligations may prioritize interest payments over dividends during tough times. Rising interest rates can further increase financial pressure. Low or manageable debt levels provide flexibility and improve dividend reliability.

4) Commodity Prices: Falling prices can reduce profits

Metal and mining companies are highly dependent on global commodity prices. A decline in prices of zinc, aluminium, or iron ore can directly impact revenue and margins. This, in turn, affects the company’s ability to maintain dividend payouts.

In addition to these factors, investors should also track management commentary, capital allocation strategy, and long-term demand outlook. A sustainable dividend is not just about current yield but about consistency across economic cycles.

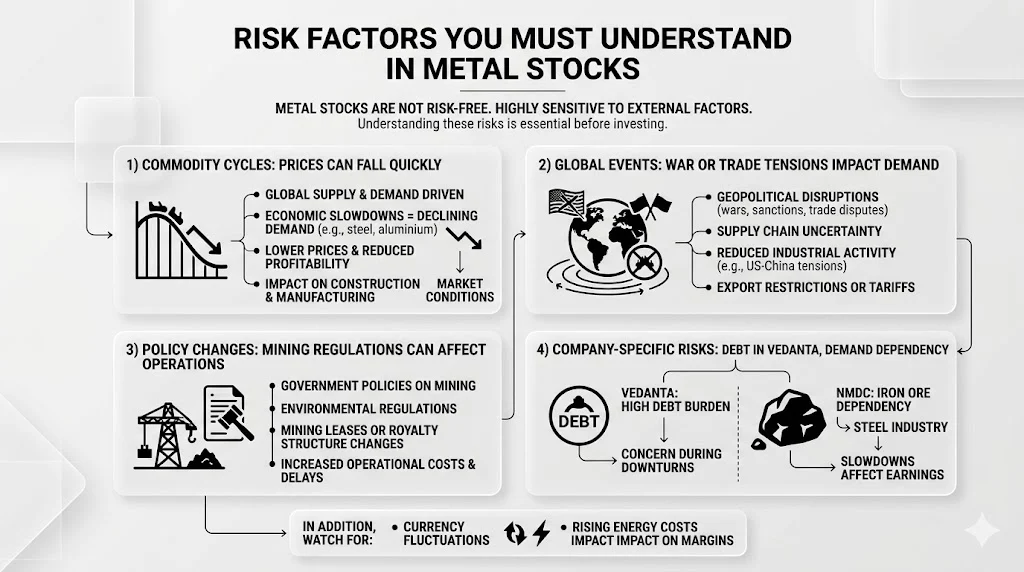

Risk Factors You Must Understand

Metal stocks are not risk-free. While they can generate strong returns during favorable cycles, they are highly sensitive to external factors that are often beyond the control of individual companies. Understanding these risks is essential before investing in this sector.

1) Commodity Cycles: Prices can fall quickly

Metal prices are driven by global supply and demand. During economic slowdowns, demand for metals like steel, aluminium, and zinc declines sharply. This leads to lower prices and reduced profitability for companies. For example, a slowdown in construction or manufacturing can directly impact steel demand, affecting companies like Tata Steel and JSW Steel.

2) Global Events: War or trade tensions impact demand

Geopolitical events such as wars, sanctions, or trade disputes can disrupt supply chains and create uncertainty in global markets. For instance, tensions between major economies like the US and China can reduce industrial activity, impacting metal consumption. Additionally, export restrictions or tariffs can affect revenue for companies that rely on international markets.

3) Policy Changes: Mining regulations can affect operations

Government policies play a major role in the mining sector. Changes in environmental regulations, mining leases, or royalty structures can increase operational costs. In India, stricter environmental norms or delays in approvals can impact production timelines and profitability.

4) Company-Specific Risks: Debt in Vedanta, Demand dependency in iron ore

Each company has its own internal risks. Vedanta, for example, carries relatively high debt, which can become a concern during downturns. Similarly, companies like NMDC depend heavily on iron ore demand, which is closely linked to the steel industry. Any slowdown in steel production can directly impact their earnings.

In addition to these factors, currency fluctuations and rising energy costs can also affect margins. Investors should regularly monitor these risks and avoid overexposure to a single stock or commodity.

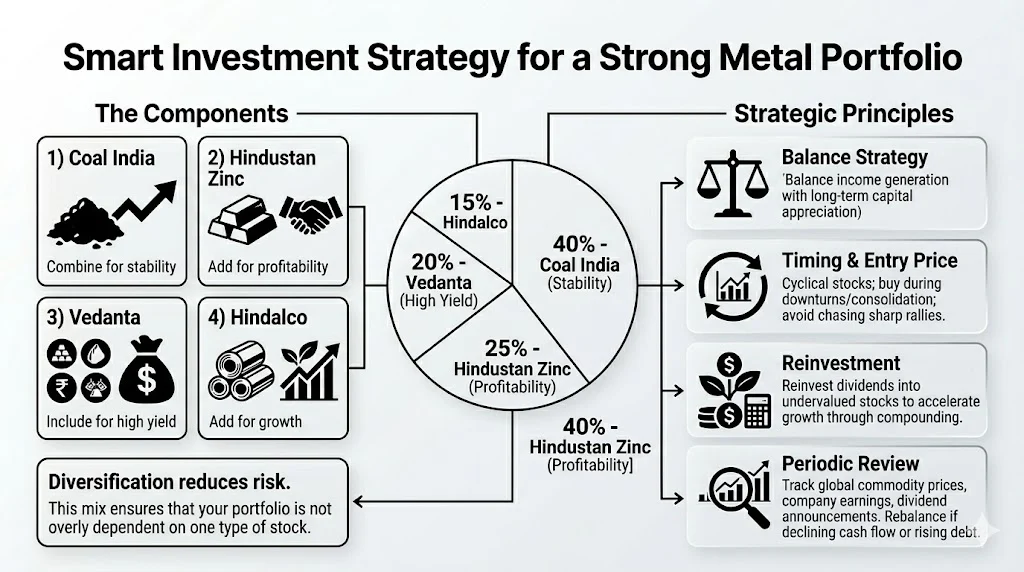

Smart Investment Strategy

To build a strong portfolio:

- Combine Coal India for stability

- Add Hindustan Zinc for profitability

- Include Vedanta for high yield

- Add Hindalco for growth

Diversification reduces risk.

However, simply selecting these stocks is not enough. A well-structured allocation strategy is equally important to maximize returns while controlling downside risk. Investors should aim to balance income generation with long-term capital appreciation.

A practical allocation approach could look like this:

- 40% in stable dividend payers like Coal India to ensure consistent income

- 25% in high profitability companies like Hindustan Zinc for strong return ratios

- 20% in high-yield stocks like Vedanta for enhanced cash flow

- 15% in growth-oriented companies like Hindalco for future upside

This mix ensures that your portfolio is not overly dependent on one type of stock. Stability stocks protect during downturns, while growth stocks help capture upside during commodity rallies.

Another important factor is timing and entry price. Metal stocks are cyclical, which means buying during downturns or consolidation phases can significantly improve long-term returns. Investors should avoid chasing stocks after sharp rallies.

Reinvestment strategy also plays a key role. Instead of withdrawing dividends, reinvesting them into undervalued stocks can accelerate portfolio growth through compounding.

Additionally, periodic review is essential. Investors should track key indicators such as global commodity prices, company earnings, and dividend announcements. If a company shows declining cash flow or rising debt, it may be wise to rebalance the portfolio.

In summary, a strong metal dividend portfolio is not just about picking the right stocks. It is about combining stability, yield, and growth with disciplined allocation and regular monitoring.

Public Sentiment and Market Behavior (Data From X)

Investors are actively discussing these stocks across multiple platforms such as financial forums, brokerage reports, and social media communities. The interest is not just limited to dividend yield but also includes long-term sustainability, commodity outlook, and company-specific developments.

Coal India continues to be trusted for steady income due to its consistent dividend payouts, strong cash reserves, and dominant position in the domestic coal market. Many investors consider it a core holding for passive income portfolios, especially those seeking low volatility.

Vedanta remains popular for high dividends, often attracting income-focused investors who are willing to accept higher risk. Discussions around Vedanta frequently include its debt levels, corporate restructuring plans, and the potential impact of its proposed demerger. While the dividend yield is attractive, investors are closely monitoring financial stability.

Hindustan Zinc is increasingly being recognized as a hidden gem. Its exceptionally high return ratios, strong balance sheet, and consistent profitability make it appealing for both dividend and quality-focused investors. Many analysts highlight its ability to generate strong free cash flow even during moderate commodity cycles.

Steel stocks such as Tata Steel and JSW Steel are being watched more for growth potential rather than dividend income. Investors are tracking global steel demand, infrastructure spending, and export opportunities. These stocks are often discussed in the context of cyclical recovery and long-term expansion.

Overall, sentiment remains positive but cautious. Investors are optimistic about dividend income opportunities but are also aware of risks such as commodity price fluctuations, global economic uncertainty, and company-specific challenges. This balanced outlook reflects a more informed and strategic approach toward investing in the metal and mining sector.

My Final Thoughts On Metal & Mining Dividend Stocks

Metal and mining dividend stocks can be a really rewarding space if you approach them with the right mindset. They give you a rare combination of steady income and the chance to benefit from growth when the cycle turns in your favor.

But honestly, this is not a sector where you can invest blindly. Prices move with global trends, and things can change quickly. So it’s important to stay aware, understand the business, and not get carried away by just high dividend numbers.

If I had to share one simple piece of advice, it would be this — focus on balance. Don’t chase only the highest yield. Instead, build a mix of stability, strong fundamentals, and income. That’s what really works over time.

For example, Coal India can give you that sense of stability. Hindustan Zinc adds strength with solid fundamentals. Vedanta can boost your income with higher payouts. When you combine them thoughtfully, you create something much more reliable than just picking one stock.

At the end of the day, investing is personal. Take your time, understand what suits your goals, and build gradually. If you stay patient and informed, this sector can quietly become a strong and dependable income source in your portfolio.

Related Posts :

Share This Post