Why CG Power Is Falling: Complete Analysis, Investment Outlook & Future Prospects

Why CG Power Is Falling | Image Via © business-standard.com

CG Power and Industrial Solutions Limited has become one of the most discussed stocks in the Indian power equipment sector. The company that delivered a spectacular turnaround story under the Murugappa Group is now facing significant selling pressure. Many investors who bought into the growth story are now asking why CG Power is falling and whether this decline presents a buying opportunity or signals deeper problems.

The stock has shown considerable volatility in recent months. From trading near highs of over ₹700, it has corrected to levels around ₹655 in late March 2026. This decline has not happened in isolation. Multiple factors ranging from order cancellations to earnings misses and valuation concerns have combined to create sustained selling pressure.

This comprehensive analysis examines why CG Power is falling, evaluates whether it is good to buy a CG Power share at current levels, and explores what the future holds for this industrial major. We will look at the technical breakdown, fundamental strengths, growth drivers, risks, and the overall investment thesis to help you make informed decisions.

Table of Contents

Current Market Position: Understanding Where CG Power Stands

Before diving into the reasons for the decline, it is important to understand CG Power’s current market position. The company operates in three main segments: Power Systems, Industrial Systems, and the newly emerging Semiconductor business through its OSAT facility.

The stock has delivered impressive long-term returns. From near bankruptcy levels of around ₹4 in 2019, it surged to over ₹700 by early 2026. This represents a return of over 175 times for early investors who believed in the turnaround story. However, recent months have seen a different narrative unfold.

As of late March 2026, the stock trades around ₹655 levels after experiencing weekly declines of 1% to 4% in multiple sessions. The year-to-date performance shows a decline of approximately 13%, significantly underperforming the broader Sensex which has fallen only about 2% in the same period.

The market capitalization remains substantial at over ₹40,000 crore, reflecting the scale of operations the company has built. However, the high valuation multiples that once justified the premium are now under scrutiny as growth shows signs of moderation.

Why CG Power Is Falling: Six Major Reasons Explained

Understanding why CG Power is falling requires examining multiple interconnected factors. Each of these reasons has contributed to the selling pressure, and together they have created a challenging environment for the stock.

1. Major Order Cancellation in Railway Segment

The most significant trigger for the recent decline was the cancellation of a major railway order worth approximately ₹500 to ₹600 crore. This order was awarded to CG Power’s subsidiary G.G. Tronics India for supplying Loco Kavach railway safety systems to Chittaranjan Locomotive Works.

The cancellation occurred because product approvals from ISA, RDSO, and compliance with Version 4.0 specifications were delayed beyond the 12-month delivery window. The company could not supply the systems within the required timeframe due to these pending approvals.

This cancellation had immediate market impact. The stock fell 2% to 7% in sessions following the announcement. Investors became concerned about execution risks in the railway segment, which had been viewed as a stable growth driver.

The railway order cancellation raises broader questions about CG Power’s ability to navigate complex regulatory approval processes. Government contracts often involve lengthy clearance timelines, and the company’s inability to meet delivery schedules despite these challenges suggests potential gaps in project planning and risk assessment.

The market reaction was severe because railway orders were expected to provide steady revenue visibility. The Kavach system is a critical safety technology for Indian Railways, and CG Power’s involvement represented a significant endorsement of its technical capabilities. The loss of this order not only impacts immediate revenue but also raises doubts about future railway business prospects.

2. Q3 FY26 Earnings Miss and Profitability Concerns

The third quarter results for fiscal year 2026 disappointed market expectations on multiple parameters. While the company reported steady year-on-year growth, it missed Street estimates on profit, revenue, and margins.

The consolidated revenue stood at ₹2,922.8 crore, representing 21% year-on-year growth but only 1.6% quarter-on-quarter growth. This sequential slowdown concerned investors who expected continued momentum.

The EBITDA came in at ₹376.7 crore, up 27.8% year-on-year but down 1.2% quarter-on-quarter. The profit after tax was ₹284.4 crore, up 29.5% year-on-year but missing analyst estimates by 6% to 9%.

Several factors contributed to this earnings miss. Labour code-related costs increased operating expenses. The Industrial Systems segment faced particular margin pressure due to project deferrals and higher commodity costs. The railways segment within Industrial Systems showed muted execution.

The market always reacts strongly to earnings misses, especially for high-growth stocks trading at premium valuations. Even small disappointments can trigger significant selling as investors recalibrate growth expectations.

The earnings miss highlighted a disconnect that has been building in CG Power’s financials. Revenue has grown from approximately ₹3,000 crore in fiscal year 2021 to over ₹9,900 crore in fiscal year 2025. However, net profit and earnings per share have not kept pace proportionally. This divergence between top-line growth and bottom-line delivery has created bearish sentiment among some analysts.

3. Extreme Valuation Multiples Creating Downside Risk

Valuation concerns represent a structural challenge for CG Power. The stock trades at price-to-earnings ratios of 75x to 80x, significantly higher than the sector average of approximately 35x to 40x.

This valuation premium was justified during the rapid growth phase when revenue was expanding at over 30% annually and the turnaround story was unfolding. However, as growth naturally moderates and execution challenges emerge, sustaining such high multiples becomes difficult.

The price-to-book ratio stands at approximately 13.8x, again indicating significant premium pricing. When compared to peers like Siemens or ABB, CG Power’s valuation appears stretched despite its faster growth rate.

Brokerage firms have taken note of these valuation concerns. Nomura trimmed earnings per share estimates by 7% to 9% for fiscal years 2026 through 2028 due to commodity headwinds and potential margin recovery challenges. The high valuation leaves little room for error, and any execution miss results in sharp corrections.

The market is essentially repricing CG Power from a high-growth, high-multiple stock to a more mature industrial company deserving moderate valuation. This repricing process is painful for existing investors but may create better entry points for new investors.

4. Commodity Price Volatility and Margin Compression

Raw material costs represent a significant challenge for CG Power’s margin profile. The company relies heavily on copper, aluminum, and steel for its power equipment and industrial systems manufacturing.

Copper prices have shown sharp volatility, with significant increases in recent months affecting input costs. Since CG Power operates in competitive markets with limited pricing power, passing these cost increases to customers becomes challenging.

The Industrial Systems segment has been particularly affected by commodity inflation. This segment reported margin contraction of 460 basis points to 8.9% in recent quarters, compared to higher levels in previous periods.

The price realization environment has remained muted despite higher input costs. This combination of rising costs and stable pricing creates margin squeeze that directly impacts profitability.

The commodity pressure is not unique to CG Power but affects the entire electrical equipment industry. However, CG Power’s high valuation means it has less margin for error compared to peers trading at lower multiples.

5. Competitive Threats and Sector-Level Concerns

The power equipment sector faces potential disruption from changing government policies regarding Chinese participation in contracts. Reports suggest that restrictions on Chinese firms bidding for government contracts may be relaxed.

Chinese companies can offer equipment at steep discounts due to scale advantages and government subsidies. If they re-enter the Indian government contract space, companies like CG Power may face significant pricing pressure.

This competitive threat creates uncertainty about future order wins and margin sustainability. The government’s push for self-reliance and domestic manufacturing provides some protection, but pricing pressure from global competitors remains a real risk.

The sector has also seen overall softness due to project deferments and delayed capital expenditure decisions by utilities and industrial customers. This demand-side weakness compounds the challenges CG Power faces.

6. Technical Breakdown and Weak Chart Patterns

From a technical analysis perspective, CG Power has shown significant weakness. The stock is trading below all key moving averages including the 5-day, 20-day, 50-day, 100-day, and 200-day moving averages.

This pattern of trading below all major moving averages typically indicates bearish technical outlook in the short term. Momentum indicators such as MACD, Bollinger Bands, and KST have all pointed to sustained downward pressure.

The stock experienced a nine-day consecutive decline in January 2026, resulting in cumulative losses of 13.74%. Such extended down moves indicate strong selling pressure and weak buyer interest.

Delivery volumes have declined sharply, with a 68% drop compared to five-day averages in some sessions. This reduction in investor participation suggests that institutional and retail buyers are staying on the sidelines.

The technical breakdown has created a self-reinforcing cycle where weak charts lead to selling by traders, which further weakens the technical position. Breaking this cycle will require either a significant positive catalyst or exhaustion of selling pressure.

Public Sentiment & Market Perception (Data Taken From X)

Understanding market sentiment provides valuable context for why CG Power is falling and where it might find support. Social media discussions on platforms like Twitter show mixed but generally cautious sentiment.

Short-term traders express bearish views based on technical weakness. Comments highlight heavy selling, bearish sentiment dominance, and weak technical indicators below key levels. These traders recommend avoiding long positions until trends reverse.

Long-term investors maintain more optimistic perspectives. Many users highlight the remarkable turnaround from near bankruptcy in 2019 to current scale. They point to massive order wins in transformers and the semiconductor opportunity as reasons to look beyond short-term volatility.

Common sentiment themes include viewing corrections as temporary or buying opportunities. Many retail investors who have held through previous cycles express confidence in the underlying business despite price weakness.

Some investors share personal journeys of holding from low levels and express belief in recovery to higher price targets. Analyst price targets from firms like UBS in the ₹900 range provide reference points for these optimistic views.

The overall tone remains cautious in the short term with continued belief in long-term structural growth. This divergence between short-term technical weakness and long-term fundamental confidence creates the volatility currently being experienced.

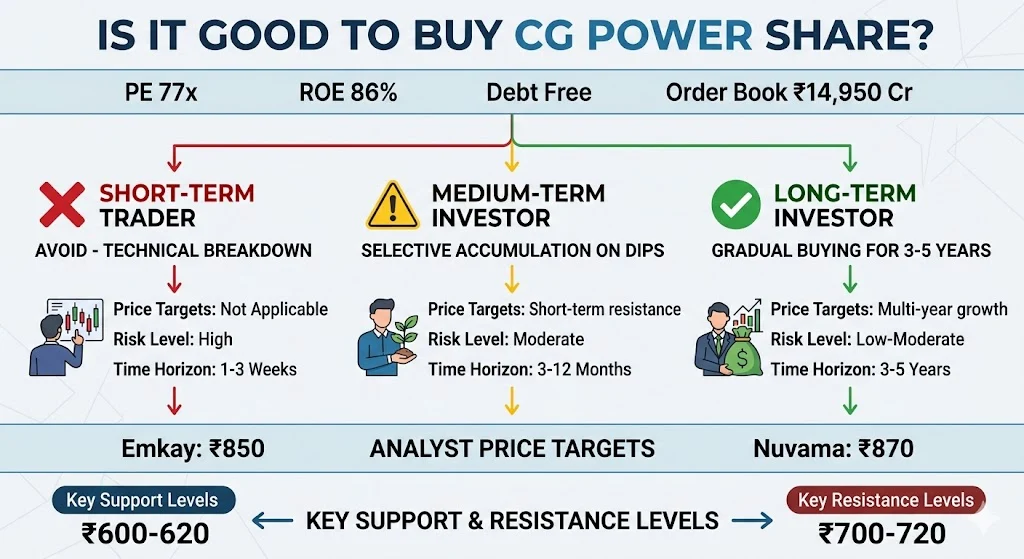

Is It Good to Buy a CG Power Share? Investment Analysis

The question of whether it is good to buy a CG Power share requires careful evaluation of multiple factors. Current market conditions present both opportunities and risks that investors must weigh based on their time horizon and risk tolerance.

The Bull Case: Reasons to Consider Buying

Several factors support the argument that CG Power represents a good buying opportunity at current levels after the recent correction.

The long-term growth story in Indian power infrastructure remains intact. The government’s focus on energy transition, renewable energy integration, and grid modernization creates sustained demand for CG Power’s core products including transformers, switchgear, and power systems.

The company’s order book stands at approximately ₹14,950 crore, representing 1.5 times fiscal year 2025 sales. This provides strong revenue visibility for the coming quarters despite recent execution challenges.

CG Power maintains a debt-free balance sheet with low debt-to-EBITDA ratio of 0.32 times. This financial strength provides flexibility to navigate cyclical downturns and invest in growth opportunities without balance sheet stress.

The return on equity has averaged an impressive 85.95% over recent periods, indicating highly efficient capital utilization. This metric demonstrates that management is effectively deploying shareholder capital to generate returns.

The semiconductor opportunity through the OSAT facility represents a significant long-term growth driver. With ₹8,000 crore investment in the Sanand facility, CG Power is positioning itself at the forefront of India’s semiconductor ecosystem. This diversification reduces dependence on traditional power equipment cycles.

Export opportunities are expanding with recent wins including US power transformer orders. The global energy transition creates demand for Indian manufacturing capabilities in power equipment.

Capacity expansion plans include doubling motors and switchgear capacity and tripling transformer capacity. These investments position the company to capture growing demand as infrastructure spending accelerates.

The Bear Case: Reasons for Caution

Several factors suggest caution before buying CG Power shares at current levels. The valuation remains elevated even after the recent correction. At 75x to 80x price-to-earnings ratio, the stock prices in very optimistic growth assumptions. Any further execution misses could lead to additional sharp corrections.

The earnings miss pattern raises concerns about management’s ability to deliver consistent results. The gap between revenue growth and profit growth suggests underlying business model challenges that may persist.

The railway order cancellation indicates execution risks in complex government projects. If similar issues arise in other large orders, the impact on revenue and reputation could be significant.

Commodity price volatility remains an ongoing challenge. With limited pricing power, margin pressure may continue until commodity cycles turn favorable or the company achieves greater scale efficiencies.

Competition from Chinese manufacturers and domestic peers like Siemens, ABB, and Hitachi Energy is intensifying. Market share protection will require sustained investment and competitive pricing.

The technical trend remains bearish with no clear signs of reversal. Buying into a falling knife can lead to further losses before any recovery materializes. Institutional investors hold 29.28% stake, which provides some confidence but also creates risk if these investors decide to reduce positions. Large block sales by institutions could drive further price declines.

Investment Recommendation by Investor Type

Different investor types should approach CG Power differently based on their objectives and risk capacity. For short-term traders, CG Power is currently not attractive. The technical breakdown, weak momentum, and bearish chart patterns suggest further downside possible. Traders should wait for clear trend reversal signals before considering entry.

For medium-term investors with 12 to 24 month horizon, selective accumulation may be appropriate. Buying in small tranches on significant dips with strict stop losses can build positions for eventual recovery. However, position sizing should be conservative given volatility.

For long-term investors with 3 to 5 year horizon, current levels may offer reasonable entry points. The semiconductor story, power infrastructure growth, and company’s execution track record support patient capital deployment. Dollar-cost averaging over several months can reduce timing risk.

For existing investors holding at higher levels, partial profit booking on any rallies makes sense to reduce exposure. Holding core positions while trimming on strength can manage risk while maintaining upside optionality.

Price Targets and Key Levels

Analyst price targets provide reference points for evaluating entry and exit decisions. Emkay Global Financial Services has a target of ₹850 with an Add rating, down from previous Buy rating. This represents approximately 30% upside from current levels.

Nuvama Institutional Equities maintains a Buy rating with target of ₹870, citing strength in Power Systems and semiconductor opportunities.

Technical support levels to watch include ₹600 to ₹620 range, which represents previous consolidation zones. A break below this level could see further decline to ₹550 or lower. Resistance levels include ₹700 psychological barrier and the 200-day moving average currently around ₹720. Sustainable recovery requires clearing these levels with volume.

What Is the Future of CG Power? Long-Term Outlook

Understanding what the future holds for CG Power requires examining growth drivers, strategic initiatives, and potential challenges over the medium to long term.

Growth Drivers and Opportunities

The future of CG Power is shaped by several powerful structural trends in the Indian and global economy. The energy transition toward renewable energy creates massive demand for power infrastructure. Solar and wind energy integration requires extensive grid modernization, transformers, and switchgear where CG Power has established capabilities.

Data center growth in India and globally drives demand for specialized power solutions. CG Power has secured orders in this segment and is expanding capacity to serve this high-growth market.

The government’s production-linked incentive schemes for semiconductors provide policy tailwinds for the OSAT facility. As one of India’s first semiconductor assembly and test facilities, CG Power is positioned to capture significant value in this emerging sector.

Railway electrification and safety system upgrades including Kavach represent long-term opportunities despite recent setbacks. The underlying demand for railway infrastructure remains strong.

Export markets in the Middle East, Africa, and Americas offer growth beyond domestic boundaries. Recent US transformer orders demonstrate capability to compete globally.

Industrial automation and digitalization trends support the Industrial Systems segment. As Indian manufacturing modernizes, demand for motors, drives, and automation solutions should grow.

Strategic Initiatives and Execution Roadmap

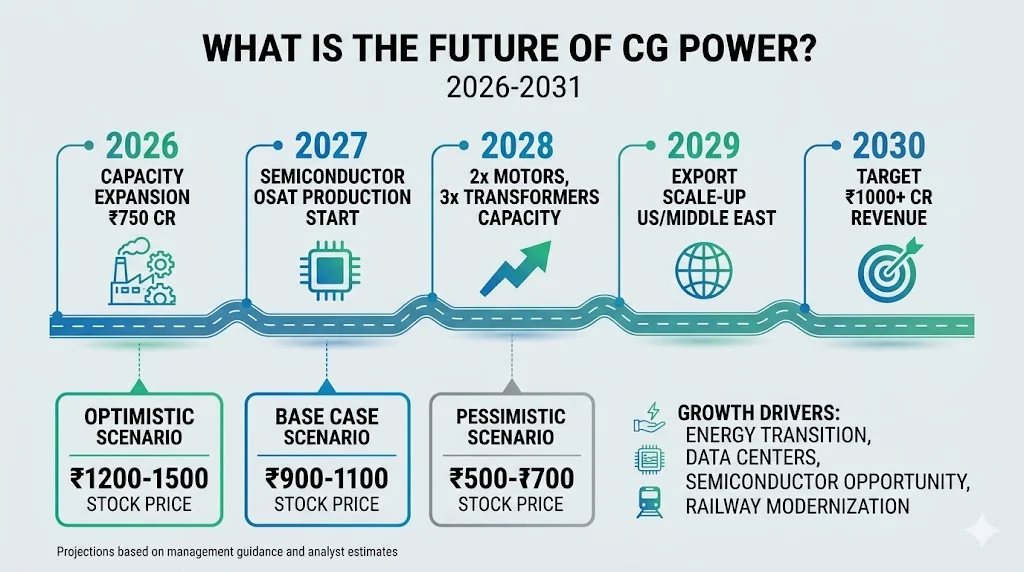

CG Power’s management has outlined clear strategic priorities that will shape the company’s future. The ₹750 crore capital expenditure plan for expanding switchgear capacity targets both domestic and export markets. This investment will increase manufacturing capabilities to meet growing order book.

The semiconductor OSAT facility in Sanand represents the most significant strategic bet. With ₹8,000 crore investment, this facility aims to tap into India’s semiconductor self-reliance goals and global supply chain diversification.

Capacity doubling in motors and switchgear and tripling in transformers will significantly increase production capabilities. These expansions prepare the company for anticipated demand growth.

Management has guided for continued strong return ratios and aims to maintain ROE above 30% despite scale challenges. This focus on capital efficiency distinguishes CG Power from competitors making less disciplined growth investments.

Potential Challenges and Risks

The future is not without significant risks that could derail growth expectations. Execution risk on large projects remains elevated. The railway order cancellation demonstrates that complex projects with regulatory dependencies can face delays and cancellations.

Margin sustainability is uncertain given commodity volatility and competitive pricing pressure. The Industrial Systems segment margin decline to 8.9% raises questions about long-term profitability in this business.

The semiconductor venture involves technology and market risks. As a new entrant in a complex global industry, CG Power faces learning curve challenges and competition from established players.

Chinese competition in government contracts could intensify if policy restrictions ease. This would pressure pricing and market share in the domestic market.

Economic cyclicality affects capital expenditure decisions by utility and industrial customers. Any slowdown in infrastructure spending would directly impact order inflows.

Valuation derating risk persists if growth moderates to 15% to 20% range from previous 30% plus levels. Multiple compression could offset earnings growth in share price performance.

Five-Year Future Scenario

Looking ahead five years to 2031, several scenarios are possible for CG Power. In the optimistic scenario, the semiconductor business achieves scale and profitability, power systems continue growing at 20% plus annually, and margins expand through scale and mix improvement. The stock could reach ₹1,200 to ₹1,500 levels representing significant upside.

In the base case scenario, power systems grow at 15% to 18%, industrial systems stabilize with modest margin recovery, and semiconductors contribute meaningfully by year four or five. The stock could reach ₹900 to ₹1,100 range.

In the pessimistic scenario, execution challenges persist, competition intensifies, and semiconductors face delays or losses. Growth moderates to 10% to 12% and margins remain under pressure. The stock could trade in ₹500 to ₹700 range with significant volatility.

The most likely outcome appears to be between base and optimistic scenarios, with success heavily dependent on semiconductor execution and maintaining power systems growth momentum.

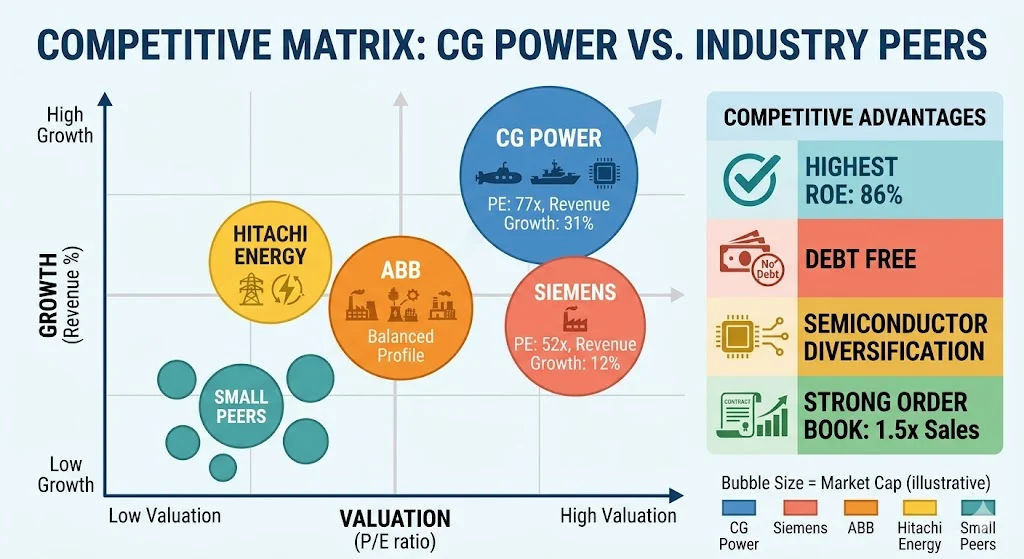

Comparative Analysis: CG Power vs Peers

Evaluating CG Power requires comparison with competitors to understand relative positioning.

CG Power vs Siemens India

Siemens India trades at lower valuations of approximately 50x to 55x price-to-earnings ratio compared to CG Power’s 75x to 80x. Siemens has more diversified portfolio including healthcare and industrial automation beyond power equipment.

Siemens offers more stable execution history but lower growth rates of 10% to 15% versus CG Power’s 20% plus. For investors prioritizing stability, Siemens may be preferable. For growth-oriented investors, CG Power’s premium may be justified if execution improves.

CG Power vs ABB India

ABB India similarly trades at valuation discount to CG Power with more mature business profile. ABB’s robotics and automation exposure provides different growth vectors.

ABB has stronger global parent support and technology access but less aggressive India-specific growth strategy. CG Power’s focused India play and Murugappa Group backing offer different risk-reward profile.

CG Power vs Hitachi Energy India

Hitachi Energy represents pure-play power equipment competitor with strong technology credentials. Recent declines in Hitachi Energy stock due to Chinese competition fears affect sector sentiment including CG Power.

Hitachi’s global technology leadership versus CG Power’s cost-competitive Indian manufacturing create different positioning. Both face similar sector headwinds currently.

CG Power vs Transformers and Rectifiers India

Smaller peers like Transformers and Rectifiers trade at lower valuations but lack CG Power’s scale, balance sheet strength, and diversification. CG Power’s premium reflects these quality differences.

Financial Health and Balance Sheet Strength

CG Power’s financial position provides important context for investment decisions. The company maintains net cash position with debt-to-equity ratio near zero. This conservative capital structure provides significant strategic flexibility.

Working capital management has improved under Murugappa ownership with better inventory and receivables management. However, large projects can create working capital swings that affect quarterly cash flows.

Capital allocation has been disciplined with investments focused on high-return opportunities like semiconductors and data center capacity. No value-destroying diversification has occurred.

Free cash flow generation has been positive despite growth investments, demonstrating earnings quality. However, the heavy capital expenditure phase for semiconductors will test cash generation in coming years.

Return on capital employed remains industry-leading at over 50%, indicating that growth investments are creating value rather than destroying it.

Risk Factors: What Could Go Wrong

Investors must understand specific risks that could make CG Power a poor investment despite apparent opportunities.

Concentration risk in large orders creates volatility. The railway order cancellation impact demonstrates how single order outcomes can affect sentiment and financials. Regulatory and approval risks are significant in Indian infrastructure. Delays in environmental clearances, safety certifications, and government payments can disrupt execution.

Technology obsolescence risk in power equipment requires continuous R&D investment. Transition to new technologies like solid-state transformers could disrupt existing capabilities. Customer concentration in utilities and government entities creates payment and order flow risks. Any slowdown in government capital expenditure directly impacts CG Power.

Foreign exchange risk affects import costs and export revenues. Rupee volatility can impact margins unpredictably. Management transition risk exists given dependence on Murugappa Group leadership. Any leadership changes could affect execution culture.

Valuation risk remains the most immediate concern. Even strong businesses can deliver poor investment returns if bought at excessive valuations.

Conclusion: Making the Investment Decision

The question of why CG Power is falling has multiple answers. Order cancellations, earnings misses, high valuation, commodity pressure, competitive threats, and technical breakdown have combined to create a challenging environment.

Whether it is good to buy a CG Power share depends on individual circumstances. The long-term story remains compelling with semiconductors, power infrastructure growth, and strong execution track record. However, short-term risks are significant and further downside cannot be ruled out.

What the future holds includes both substantial opportunity and material risk. The next two years will be critical in determining whether CG Power can transition from a high-growth turnaround to a sustainably profitable industrial major.

For investors with long-term horizon and risk tolerance, current levels may offer reasonable entry points with appropriate position sizing. For those seeking immediate returns or unable to tolerate volatility, waiting for clearer trend reversal makes sense.

The key is distinguishing between short-term noise and long-term value creation. CG Power has demonstrated remarkable transformation capabilities. Whether it can execute the next phase of growth while managing valuation expectations will determine investment outcomes.

Understanding your own investment objectives, time horizon, and risk tolerance is essential before making any decision. This analysis provides the framework for that decision but cannot replace individual judgment about suitability.

Quick Reference Summary

| Parameter | Current Status |

|---|---|

| Stock Price | Around ₹655 |

| 52-Week High | ₹749 |

| 52-Week Low | ₹560 |

| Market Cap | ₹40,000+ crore |

| PE Ratio | 75x to 80x |

| PB Ratio | 13.8x |

| ROE | 85% (historical average) |

| Debt to Equity | Near zero |

| Order Book | ₹14,950 crore |

| Analyst Targets | ₹850 to ₹870 |

Frequently Asked Questions

Q1: Why is CG Power falling despite strong revenue growth?

A: The fall is driven by earnings misses, order cancellations, high valuation compression, and margin pressures that have disappointed investors expecting flawless execution.

Q2: Is it good to buy CG Power share now or wait?

A: Long-term investors may consider gradual accumulation on dips, while short-term investors should wait for trend reversal confirmation. Position sizing should reflect risk tolerance.

Q3: What is the future of CG Power’s semiconductor business?

A: The OSAT facility represents significant long-term opportunity but involves execution risks. Success could transform the company, while delays would disappoint expectations.

Q4: How does CG Power compare to Siemens and ABB?

A: CG Power offers higher growth but higher valuation and execution risk. Peers provide more stability but lower growth potential.

Q5: What price levels should investors watch?

A: Support at ₹600 to ₹620 and resistance at ₹700 to ₹720 are key technical levels. Fundamental value likely exists between ₹550 and ₹650 range.

Related Posts :

Share This Post